Day Hagan Smart Sector® Fixed Income Strategy Update June 2026

A downloadable PDF copy of the Article:

Day Hagan Smart Sector® Fixed Income Strategy Update June 2026 (pdf)

Executive Summary

Global fixed income markets were choppy in May as investors balanced elevated inflation, slower labor momentum, Treasury supply, and shifting geopolitical risk. The Federal Reserve held the federal funds target range at 3.50% to 3.75% at its late-April meeting, and the minutes released in May showed policymakers focused on inflation risk, energy prices, tariffs, and uncertainty in the Middle East.

Economic data released during the month complicated the rate outlook. April payrolls increased by 115,000, while the unemployment rate held at 4.3%. April CPI rose 3.8% from a year earlier, and core CPI rose 2.8%. The Fed’s preferred PCE gauge also moved higher, with headline PCE at 3.8% and core PCE at 3.3%. Because the May employment and inflation reports were not available by month-end, investors were left trading on April data and forward-looking inflation concerns.

Treasury markets were pressured by the combination of sticky inflation and large financing needs. Treasury’s May refunding kept nominal coupon and floating-rate note auction sizes unchanged for the May-July quarter, but also indicated greater reliance on bills later in May. Auction demand was mixed. The 10-year note sale drew below-average demand, while the 30-year bond auction cleared above 5%, a reminder that investors continued to require compensation for fiscal, inflation, and duration risk. We remain neutral on 3-7-year and 10-20-year Treasuries, as income is more attractive, but long-end volatility remains a constraint.

Short-term TIPS remain underweight because near-term inflation compensation already reflects much of the energy shock, and real-rate volatility remains elevated. Agency MBS remain underweight due to rate volatility and spread sensitivity. Floating-rate exposure is neutral, helped by high short rates but with less upside if growth cools.

Credit held up better than duration-heavy segments, as investor demand for income supported U.S. investment-grade corporates and high-yield, both of which remain overweight. International corporates remain underweight given currency risk, slower regional growth, and policy divergence. Emerging-market bonds remain overweight, supported by carry and selective easing by central banks. Looking ahead, May payrolls, May CPI, June Fed guidance, oil prices, and demand for longer-maturity auctions should drive the next phase.

Holdings

Fixed Income Sector

US 1-3 Month T-bill

US 3-7 Year Treasury

US 10-20 Year Treasury

TIPS (short-term)

US Mortgage-Backed

US Floating Rate

US Corporate

US High Yield

International Corporate Bond

Emerging Market Bond

Outlook (relative to benchmark)

Overweight

Neutral

Neutral

Underweight

Underweight

Neutral

Overweight

Overweight

Underweight

Overweight

Position Details

U.S. Treasuries: The Treasury indicator backdrop is mixed, supporting our neutral stance across 3-7-year and 10-20-year Treasuries. The U.S. Long Treasury indicators show bearish readings from the technical cross and credit default swap signals, but bullish readings from technical momentum, equity-market trend, and inflation expectations. That combination suggests Treasuries are still useful as portfolio ballast, but not compelling enough for an overweight while long-end volatility, fiscal supply, and inflation uncertainty remain elevated.

May was shaped by three dominant forces: sticky inflation, Fed patience, and Treasury financing needs. April CPI accelerated to 3.8% year over year, while April PCE also reached 3.8%. Those readings kept investors cautious about duration and reduced confidence that the Fed could ease soon. The Fed held the target range at 3.50% to 3.75%, and the April meeting minutes released in May showed policymakers focused on energy prices, tariffs, and whether inflation would remain above target for longer.

Supply also mattered. Treasury kept nominal coupon auction sizes unchanged for the May-July quarter, but financing needs remained large, and bill issuance was expected to rise later in May. The 20-year auction cleared at a yield above 5%, underscoring the extra compensation investors demanded for long-maturity risk. At the same time, yields fell late in the month as oil prices eased and hopes for calmer Middle East headlines reduced inflation fears.

Going forward, the key issues are May payrolls and CPI released in June, the June Fed message, oil prices, and long-end auction demand. We prefer a balanced Treasury posture rather than aggressively extending duration.

Figure 1: A reversal lower for inflation expectations would potentially support fixed-income holdings.

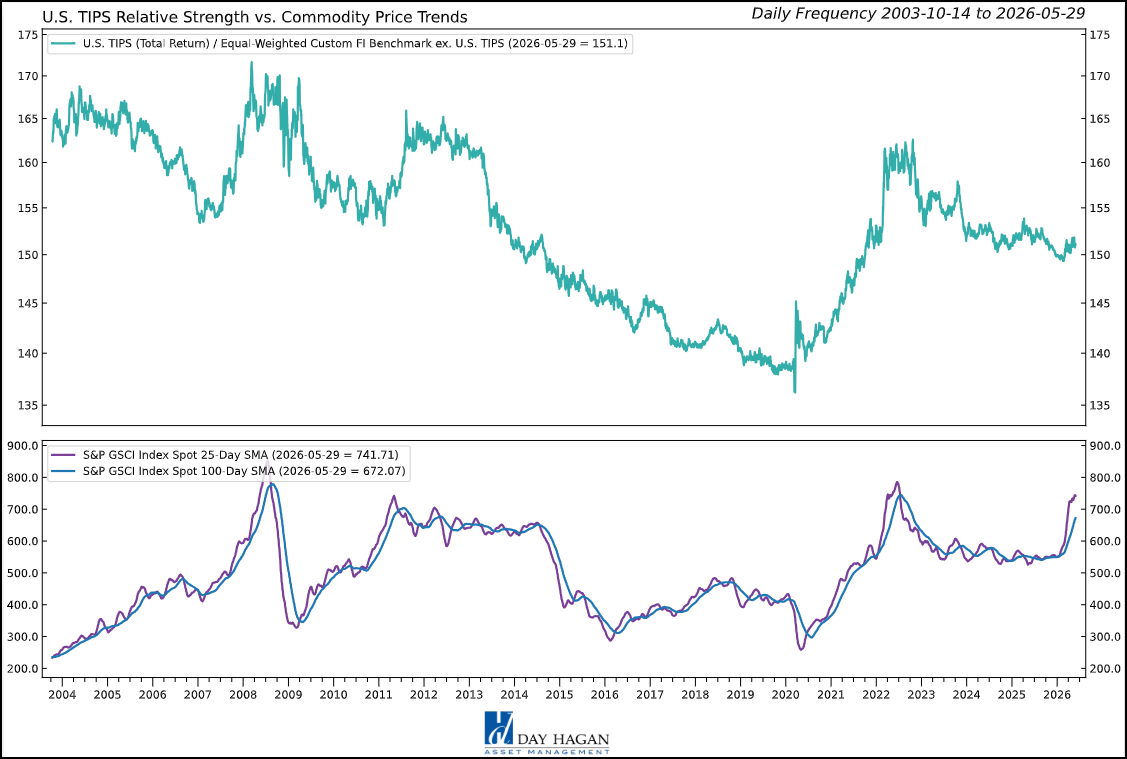

U.S. TIPS: The short-term TIPS indicator set remains unfavorable. Five of the six readings are bearish, including technical RSI, momentum mean reversion, moving average cross, high-yield OAS, and inflation expectations. The only bullish signal is commodity price trends. That mix argues that inflation-linked bonds may benefit from energy and commodity volatility, but that the market has already priced in a meaningful amount of near-term inflation risk.

The macro case for TIPS is not weak, but the valuation and timing case is less attractive. April CPI rose 3.8% year over year, driven by energy, shelter, and other cost pressures, while April PCE also rose 3.8%. Those figures reinforced the inflation hedge argument. However, short-term TIPS are especially sensitive to the path of realized inflation versus what is already embedded in breakevens. With energy prices already pushing inflation expectations higher, the hurdle for additional upside has increased.

Fed policy adds another complication. The Fed held rates at 3.50%-3.75%, and officials indicated that tariffs and energy prices were important sources of inflation uncertainty. If inflation cools because energy prices stabilize, short-term TIPS could lose support. If inflation remains high, real yields may also remain elevated, limiting total return potential. Treasury also kept TIPS auction sizes unchanged for May-July, including the May 10-year reopening, June 5-year reopening, and July 10-year new issue. That steady supply profile does not create a major technical tailwind.

For clients, short-term TIPS remain a useful hedge, but not our preferred inflation-sensitive exposure today. We would look for better entry points if breakevens cheapen, real yields stabilize, or the indicator profile improves.

Figure 2: A peak in commodity prices would potentially create headwinds for TIPS.

U.S. Mortgage-Backed Securities: The MBS indicator set remains cautious. Moving average cross, relative-strength slope, and high-yield OAS readings are bearish, while RSI and the 10-year yield signal are bullish. Inflation expectations are neutral. This split suggests MBS has some tactical support when rates stabilize, but the broader trend and relative-strength profile still argue for an underweight.

The fundamental backdrop is challenging. Mortgage rates remained elevated in May, with Freddie Mac reporting the 30-year fixed rate at 6.53% as of May 28, up from 6.51% the prior week. Higher mortgage rates continued to weigh on affordability and housing activity. Mortgage applications declined in the MBA weekly survey released May 27, and new-home sales fell in April. Home prices were still supported by limited supply, but transaction activity remained constrained by borrowing costs and household budget pressure

Rate volatility is the central issue for agency MBS. Inflation data released in May pushed Treasury yields higher at times, while geopolitical headlines and oil-price moves created sharp swings in the long end. MBS can perform better when volatility falls, and late-month calmer rate action helped spreads in parts of the market. Still, the sector remains exposed to duration extension when rates rise and negative convexity when rates fall. The Fed’s balance sheet also remains a consideration, as agency MBS holdings continue to exit the private market, increasing the supply to absorb over time.

The sector offers high credit quality and attractive income versus Treasuries, but we prefer to wait for a more favorable technical setup. Watch mortgage rates, rate volatility, Fed balance sheet policy, prepayment expectations, and whether housing demand stabilizes.

Figure 3: 10-year yields appear “overbought.” A reversal back below the top bracket would generate a buy signal.

U.S. Floating Rate Notes (FLRN): The floating-rate note indicators remain broadly constructive, with bullish readings from the technical cross, technical momentum, OIS swap rate, and VIX extremes. The one caution is the relative-strength slope indicator, which is bearish and suggests that the leadership profile has begun to lose momentum. That mix fits a neutral allocation. The sector continues to benefit from a high short-rate environment, with the Federal Reserve holding the federal funds target range at 3.50% to 3.75% at its late-April meeting and Fed officials still focused on inflation risk from energy, tariffs, and geopolitics.

The macro backdrop supports income generation but limits upside. April CPI rose 0.6% month over month, driven largely by energy, food, and shelter, while April PCE inflation also moved higher. This kept front-end rates anchored and made floating-rate exposure useful as a carry tool. At the same time, May flash PMIs showed a split economy. Manufacturing improved to 55.3, the strongest reading since 2022, while services were softer at 50.9. That points to continued growth, but not broad enough acceleration to justify a more aggressive stance.

Investor demand for short and intermediate-term high-quality bond funds remained healthy in late May, supported by elevated yields and caution toward longer duration. Going forward, the key issues are whether energy-driven inflation fades, whether the Fed retains its easing bias, and whether front-end rates remain high enough to compensate for limited spread upside. Floating-rate notes still have a role, but the bearish relative-strength slope argues against an overweight.

Figure 4: Technical momentum is nearing previous overbought levels.

U.S. Investment-Grade Corporate Bonds: The outlook is constructive despite mixed indicators. Negative readings from implied bond volatility, option-adjusted spreads, technical cross, and price mean reversion. Credit default swaps and the dollar are neutral. This suggests the broader high-quality bond market is still dealing with rate volatility and less favorable spread technicals, but it does not fully offset the positive case for U.S. corporates within the fixed-income portfolio.

The main support is corporate fundamentals. FactSet reported that Q1 2026 blended S&P 500 earnings growth was 28.6% year over year as of May 29, with revenue growth of 11.8%. Earnings strength was heavily influenced by technology, communications, consumer discretionary, and AI-related investment, but the broader message for bondholders is that large U.S. issuers entered midyear with solid cash-flow coverage and access to capital. That helps explain why we remain overweight U.S. corporate bonds even while broad aggregate indicators are not uniformly favorable.

Macro data released in May were more complicated. Inflation moved higher in April, real income was pressured, and long Treasury yields were volatile as investors absorbed larger financing needs and energy-related inflation risk. Still, demand for income remained strong, and U.S. bond funds attracted inflows late in the month, including short- to intermediate-duration investment-grade strategies.

For clients, the balance is between attractive all-in yields and late-cycle risks. We prefer higher-quality issuers, sectors with earnings visibility, and structures less exposed to long-duration volatility. Watch Treasury yields, oil prices, primary-market concessions, and any deterioration in credit default swaps.

Figure 5: Credit default swap levels remain near historical lows. A rise above the lower bracket would generate a sell signal.

U.S. High Yield: The high yield indicator set is the strongest among the credit segments. All six readings are bullish, including the technical cross, high-yield breadth, small-cap equity trend, absolute total-return moving average cross, VIX moving average cross, and OAS reversal signal. That combination points to broad market participation, supportive risk appetite, and improving relative strength relative to more defensive fixed-income sectors.

Fundamentals are also supportive, though selectivity matters. FactSet’s May 29 Earnings Insight showed Q1 S&P 500 blended earnings growth of 28.6% and revenue growth of 11.8%. While high-yield issuers are not the S&P 500, the earnings backdrop, equity strength, and improved access to capital help support lower-quality credit. May equity trends were important as well, with AI and technology leadership lifting broader sentiment and helping credit spreads avoid a more damaging reaction to higher rates.

The macro backdrop still requires attention. April inflation data moved higher, the Fed remained on hold, and long Treasury yields were volatile as investors reassessed energy risk and fiscal supply. Higher borrowing costs can pressure lower-rated issuers, especially those with near-term refinancing needs. There were also warning signs in private credit, where reports of higher unrealized losses and rising payment-in-kind income indicated stress below the public high-yield market.

We remain overweight because technicals, income, and investor appetite remain favorable. Going forward, watch small-cap equity trends, high yield breadth, default expectations, private credit spillover risk, and whether oil prices keep inflation pressure high enough to delay Fed easing

Figure 6: High-yield bond breadth improving from a short-term oversold condition.

International Investment-Grade Corporate Bonds: The indicator set is uniformly bearish, with negative readings from equity risk and VIX, relative-strength slope, moving average cross, option-adjusted spread, and credit default swaps. That is a meaningful warning for international corporate bonds, especially as global credit investors face a combination of slower growth, policy divergence, currency volatility, and region-specific credit stress.

Europe is the main source of caution. Euro Area inflation was confirmed at 3.0% in April, above the European Central Bank’s 2% target, while the composite PMI fell to 47.5 in May from 48.8 in April. That points to a contraction in private-sector activity at the same time that energy-driven inflation is limiting the ECB’s flexibility. The ECB deposit rate remained at 2.0%, but officials were still focused on the persistence of the energy shock. This is not an ideal mix for corporate credit, because softer activity can weaken earnings while inflation keeps financial conditions tight.

The United Kingdom and Japan also add complexity. The Bank of England held Bank Rate at 3.75%, and the Bank of Japan kept its policy rate at 0.75%, with inflation risk and currency pressures still in focus. For U.S.-based investors, currency hedging costs and dollar volatility can meaningfully affect the realized returns on international bonds.

Investor flows also argue for caution. Global bond funds attracted inflows late in May, but the ECB noted strong outflows from high-yield corporate bond funds and highlighted pockets of stress in private credit. We remain underweight international corporate bonds until the indicators improve, PMIs stabilize, and spreads offer better compensation for currency, growth, and policy risk.

Figure 7: The long-term trend factor remains negative.

Emerging Market Bonds: The EM bond indicators are firmly bullish. Relative strength versus the EM currency index, emerging equity momentum, commodity strength, the absolute moving-average cross, and the relative-strength moving-average slope all point in the same direction. That broad confirmation supports the overweight to emerging-market bonds, particularly USD-denominated exposure, where income remains attractive, and currency risk is less direct than in local-currency debt.

Macro conditions are mixed but still supportive for selective EM credit. China’s official manufacturing PMI slipped to 50.0 in May from 50.3 in April, indicating stalled manufacturing momentum, while new export orders weakened. That is a risk for countries tied to Chinese demand. At the same time, parts of EM are still benefiting from commodity income, domestic stimulus, and easing cycles. Brazil’s economy grew 1.1% quarter over quarter in Q1, supported by consumption and investment, though persistent inflation has made the rate-cut path less certain.

Flows are an important positive. LSEG/Lipper data cited by Reuters showed emerging market bond funds gaining inflows in the week ended May 27, while EM equity funds saw outflows. That split suggests investors still value EM fixed-income carry even as they are more cautious about EM equities. The commodity backdrop is also important. Oil and energy volatility have created inflation risk, but they can support selected exporters and improve external balances.

The main risks are a stronger dollar, higher U.S. real yields, weaker demand in China, and geopolitical shocks. We favor a diversified EM USD approach, with emphasis on countries showing credible policy, manageable external financing needs, and improving current-account dynamics.

Figure 8: Positive EM equity performance often supports EM bond performance.

Catastrophic Stop Model

The Catastrophic Stop model combines time-tested, objective indicators to identify high-risk periods for equities and fixed-income assets that are highly correlated with the equity market. The model entered June recommending a fully invested allocation relative to the benchmark for credit sectors that are highly correlated with equities.

The weight of the evidence suggests that any weakness in equity is unlikely to extend into a significant downtrend at this time. Of course, if our model triggers a sell signal (below 40% for two consecutive days), indicating more substantial problems, we will reduce exposure.

Figure 9: The Catastrophic Stop model recommends a fully invested position (relative to the benchmark). Because the model uses indices to extend its history, it is considered hypothetical.

Hypothetical and historical past performance is not indicative of future results. There can be no assurance that any investment or strategy will achieve its objectives or avoid substantial losses or have comparable results. This information is provided for illustrative purposes only and is not a prediction, projection, or guarantee of future performance. Hypothetical results do not reflect actual trading, were derived using the benefit of hindsight, and may not reflect material economic and market events. Actual results vary and depend on many factors and subject to risk and uncertainties.

Our goal is to stay on the right side of the prevailing trend and introduce risk management when conditions deteriorate. Currently, the uptrend remains intact. The broader-based composite models calling U.S. economic growth, international economic growth, inflation trends, liquidity, and equity demand remain broadly constructive. The Catastrophic Stop model is positive, and we are aligned with the message. If our models shift to bearish levels, we will raise cash and lower exposure to risk-on fixed-income sectors.

This strategy uses measures of price, valuation, economic trends, liquidity, and market sentiment to make objective, rational, and unemotional decisions about how much capital to risk and where to allocate it.

For more information, please contact us at:

Day Hagan Asset Management

1000 S. Tamiami Trl

Sarasota, FL 34236

Toll Free: (800) 594-7930

Office Phone: (941) 330-1702

Website: https://dayhagan.com or https://dhfunds.com

© 2026 Day Hagan Asset Management

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

Day Hagan Smart Sector® Fixed Income ETF

Symbol: SSFI

Disclosures

The data and analysis contained within are provided “as is” and without warranty of any kind, either express or implied. The information is based on data believed to be reliable, but it is not guaranteed. Day Hagan DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY, OR FITNESS FOR A PARTICULAR PURPOSE OR USE. All performance measures do not reflect tax consequences, execution, commissions, and other trading costs, and as such, investors should consult their tax advisors before making investment decisions, as well as realize that the past performance and results of the model are not a guarantee of future results. The Smart Sector® Strategy is not intended to be the primary basis for investment decisions, and the usage of the model does not address the suitability of any particular investment for any particular investor.

Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many difficulties, and their effectiveness has significant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the effectiveness of such devices. Day Hagan believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider differing viewpoints and use a weight-of-the-evidence approach that fits their investment needs.

Past performance does not guarantee future results. No current or prospective client should assume future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client’s portfolio. Historical performance results for investment indexes and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that a portfolio will match or outperform any particular benchmark. Comparisons to indices are inherently unreliable indicators of future performance. The strategies used to generate the performance vary from those used to generate the returns depicted in the benchmarks. Investors cannot directly invest in an index.

The information contained herein is provided for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The securities, instruments, or strategies described may not be suitable for all investors, and their value and income may fluctuate. Past performance is not indicative of future results, and there is no guarantee that any investment strategy will achieve its objectives, generate profits, or avoid losses.

This material is intended to provide general market commentary and should not be relied upon as individualized investment advice. Investors should consult with their financial professional before making any investment decisions based on this information.

The material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Day Hagan Asset Management, its affiliates, employees, or third-party data providers shall not be liable for any loss sustained by any person relying on this information. All opinions and views expressed are subject to change without notice and may differ from those of other investment professionals within Day Hagan Asset Management or Ashton Thomas Private Wealth, LLC.

Accounts managed by Day Hagan Asset Management or its affiliates may hold positions in the securities discussed and may trade such securities without notice.

Day Hagan Asset Management is a division of and doing business as (DBA) Ashton Thomas Private Wealth, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training.

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved.

All hypothetical results are presented for illustrative purposes only. Back testing and other statistical analysis is provided in use simulated analysis and hypothetical circumstances to estimate how it may have performed prior to its actual existence. The results obtained from "back-testing" information should not be considered indicative of the actual results that might be obtained from an investment or participation in a financial instrument or transaction referencing the Index. The Firm provides no assurance or guarantee that the products/securities linked to the strategy will operate or would have operated in the past in a manner consistent with these materials. The hypothetical historical levels have inherent limitations. Alternative simulations, techniques, modeling or assumptions might produce significantly different results and prove to be more appropriate. Actual results will vary, perhaps materially, from the simulated returns presented.

© 2026 Day Hagan Asset Management

Disclosure

Federal Reserve (Fed) — The central bank of the United States, responsible for setting monetary policy and short-term interest rates.

U.S. Treasuries — Bonds issued by the U.S. government; they are widely used as benchmarks for interest rates and as defensive assets in portfolios.

T-bill (Treasury bill) — A short-term U.S. government security, typically maturing in one year or less.

Duration — A measure of a bond’s sensitivity to changes in interest rates; higher duration usually means greater price movement when yields change.

Yield — The income return on a bond, usually expressed as an annual percentage of its price.

Investment-Grade (IG) Corporate Bonds — Corporate bonds with relatively high credit quality and lower default risk than high-yield bonds.

High-Yield (HY) Bonds — Lower-rated corporate bonds that offer higher yields because they carry higher credit risk.

Private Credit — Non-bank lending, often directly to companies, outside the public bond markets.

TIPS (Treasury Inflation-Protected Securities) — U.S. government bonds designed to protect investors from inflation by adjusting principal based on inflation.

Breakeven Inflation Rate — The market’s implied inflation expectation, calculated as the difference between nominal Treasury yields and TIPS yields.

Real Yield — A bond yield after adjusting for inflation; often referenced in connection with TIPS.

Nominal Yield — A bond yield not adjusted for inflation.

Inflation Expectations — The market’s view of future inflation, which influences both bond yields and asset prices.

Mortgage-Backed Securities (MBS) — Bonds backed by pools of home mortgages; investors receive cash flows from underlying mortgage payments.

Agency MBS — Mortgage-backed securities issued or guaranteed by U.S. government-related agencies, generally viewed as having high credit quality.

Floating Rate Notes (FRNs) — Bonds whose interest payments reset periodically based on a short-term reference rate, reducing interest-rate sensitivity.

SOFR (Secured Overnight Financing Rate) — A key U.S. benchmark short-term interest rate used in loans, derivatives, and floating-rate instruments.

OIS (Overnight Index Swap) Rate — A rate derived from swaps tied to overnight interest rates, often used to gauge policy-rate expectations.

Primary Issuance — The sale of new bonds into the market by governments or companies.

Spread — The yield difference between one bond and a benchmark, often used to measure compensation for credit risk.

Option-Adjusted Spread (OAS) — A spread measure that adjusts for embedded bond options, commonly used in corporate bonds and mortgage-backed securities.

Credit Default Swap (CDS) — A derivative contract used to insure against bond default risk; rising CDS levels often signal greater credit concern.

Carry — The return earned from holding a bond or credit asset, assuming market conditions remain stable.

Refinancing Risk — The risk that a borrower will face higher costs or difficulty when replacing maturing debt with new debt.

Emerging Market (EM) Bonds — Debt issued by governments or companies in developing economies.

Hard-Currency Debt — Emerging-market debt issued in a major foreign currency, usually U.S. dollars or euros.

Local-Currency Debt — Emerging-market debt issued in the borrower’s domestic currency, making returns more sensitive to exchange-rate movements.

Risk-On / Risk-Off — Market environments where investors are either more willing to buy riskier assets (“risk-on”) or prefer safer assets (“risk-off”).

RSI (Relative Strength Index) — A technical indicator used to assess whether an asset may be overbought or oversold.

VIX — A widely followed measure of U.S. equity market volatility, often called the market’s “fear gauge.”