Day Hagan Smart Sector® with Catastrophic Stop Strategy Update June 2026

A downloadable PDF copy of the Article:

Day Hagan Smart Sector® with Catastrophic Stop Strategy Update June 2026 (pdf)

Executive Summary

In May, the U.S. stock market extended its advance, supported by strong corporate earnings, renewed enthusiasm for artificial intelligence, and economic data that still pointed to growth, though with less breadth beneath the surface. The S&P 500 gained roughly 5% for the month and finished May near record highs, while the Nasdaq continued to lead, driven by strength in large-cap technology, software, semiconductors, and AI infrastructure beneficiaries. However, the rally was concentrated: Information Technology was the clear leader, while most other S&P 500 sectors lagged or declined.

Corporate earnings remained the primary support for equities. According to FactSet, with 97% of S&P 500 companies having reported Q1 results, blended earnings growth was 28.6% and revenue growth was 11.8%. Information Technology, Communication Services, Materials, and Consumer Discretionary were among the leading sectors for earnings growth. FactSet also noted that 85% of companies beat EPS estimates and 81% beat revenue estimates, both above recent averages.

The macro backdrop was more mixed. First-quarter real GDP was revised down to a 1.6% annualized rate from the initial 2.0% estimate, reflecting softer consumer spending and investment. April retail sales rose 0.5%, but much of the increase was driven by gasoline and energy spending rather than broad-based real consumption strength. April CPI accelerated to 3.8% year over year, with energy prices up 17.9% and gasoline up 28.4%, keeping inflation risk central to the outlook. Core CPI rose 2.8%, while April PCE inflation increased to 3.8% year over year, and core PCE rose 3.3%.

The Federal Reserve kept the federal funds target range at 3.50%–3.75% at its April 29 meeting and reiterated a data-dependent approach. Overall, May favored companies with strong earnings, AI exposure, pricing power, and durable margins. Still, narrow market leadership, elevated inflation, higher energy costs, and Fed caution remain important risks for investors.

Sector

Consumer Discretionary

Consumer Staples

Communication Services

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Real Estate

Utilities

Outlook (relative to benchmark weighting)

Modest Overweight

Underweight

Neutral

Modestly Underweight

Underweight

Underweight

Underweight

Overweight

Underweight

Neutral

Modestly Overweight

Sector Review

The sector weightings suggest a portfolio intentionally tilted toward earnings visibility, secular growth, and balance sheet quality, while avoiding areas where relative strength, revisions, or macro sensitivity is less favorable. The overweight of Information Technology is the clearest expression of this view, reflecting the sector’s dominant earnings contribution, strong revision breadth, and continued leadership from AI, cloud, semiconductors, and software. The Utilities overweight adds a defensive, income-oriented counterbalance while also providing exposure to structural growth in electricity demand tied to data centers, electrification, and grid investment.

At the same time, the portfolio is not simply a high-beta growth allocation. The neutral weights in Communication Services and Real Estate recognize attractive opportunities but also acknowledge concentration risk in mega-cap platforms and continued rate sensitivity in REITs. The modest overweight in Consumer Discretionary reflects strong earnings momentum, but the sizing appropriately respects stretched valuations and uneven consumer conditions.

The underweights in Financials, Health Care, Industrials, Materials, Consumer Staples, and Energy indicate caution toward sectors where technical indicators, earnings revisions, valuation support, or macro fundamentals are less compelling. Overall, the weightings point to a selective, pro-growth portfolio with meaningful risk controls: participate in the market’s strongest earnings engines, but avoid overcommitting to cyclicals, defensives, or commodity-sensitive sectors without clearer confirmation.

Consumer Discretionary — Modest Overweight

The Consumer Discretionary sector offers a nuanced yet attractive opportunity. Current indicators highlight positive short- and intermediate-term relative moving averages, favorable deviation-from-trend measures, and supportive signals from consumer credit and the 30-year Treasury yield. However, these are offset by weaker relative momentum, overbought/oversold conditions, new highs, and relative forward P/E readings. This combination suggests a modest overweight—appropriate for a cautiously optimistic stance rather than a bold cyclical bet.

From a fundamental perspective, the sector delivered impressive Q1 earnings. According to FactSet, Consumer Discretionary earnings grew by about 40.8%, with Amazon accounting for a significant portion of that gain. Without Amazon, sector growth would have been 16.6%—respectable, though notably lower. Autos and broadline retail also posted robust results, while household durables and apparel/luxury segments lagged.

Macro dynamics play a key role. While April retail sales rose 0.5%, higher inflation and gasoline prices constrained discretionary spending, and consumer confidence declined in May. Softer housing activity continues to weigh on demand for home improvement, furniture, and durable goods. With the sector holding the highest forward P/E in FactSet’s data at 27.8, valuations are a headwind. Companies with pricing power, recurring demand, or exposure to travel, leisure, or platform-based business models are likely better positioned than rate-sensitive durables and segments dependent on lower-income consumers.

Figure 1: The Consumer Discretionary Sector Composite. (Note: All charts are proprietary to Day Hagan Asset Management.)

While Consumer Staples are often viewed as defensive, they are not particularly attractive in the current environment. Most sector indicators point to negative (bearish) conditions: moving-average cross, deviation from trend, net-new highs, short interest, food sales, food CPI, and sales-yield signals—though some positives persist in relative momentum, breadth, financial conditions, and economic-surprise indicators. This mix indicates Staples may offer some protection during risk-off periods, but their overall risk/reward profile is less compelling right now.

Earnings quality paints a mixed picture. FactSet data shows that while a high percentage of Staples companies surpassed EPS estimates and revenue beat rates were supportive, the aggregate revenue surprise was modest at around 1.0%. This suggests disciplined cost management rather than surging demand. With overall inflation rising to 3.8% in April and food costs still a concern for households, it remains to be seen if branded food and household products companies can maintain pricing power without hurting volumes.

Valuations and investor flows provide little support. According to FactSet, Consumer Staples have the lowest share of Buy ratings among S&P 500 sectors—just 43%—and one of the smallest projected 12-month price upsides at 11.6%. While Staples can still add stability to portfolios, an underweight position is sensible unless new data signals a more pronounced economic slowdown or a sharp decline in risk appetite.

Figure 2: The Consumer Staples Sector Composite.

Communication Services — Neutral

Communication Services stands out for its strong earnings narrative, but the current set of indicators supports a neutral, rather than an overweight, position. Relative price, moving averages, and one overbought/oversold measure are positive, as is the relative earnings-yield signal. Counterbalancing these are weaker signals in a second overbought/oversold measure, deviation from trend, and the yield-curve indicator (10-year minus 2-year).

The sector’s underlying fundamentals are strong but heavily concentrated. FactSet reports Q1 earnings growth of 48.9% for Communication Services, primarily driven by Alphabet and Meta. Without these two giants, the sector would have recorded an earnings decline instead of robust growth. Revenue grew a healthy 15.1% year over year across all five industries, with Interactive Media & Services leading at 24%.

The main takeaway is that Communication Services now revolves around mega-cap platforms, digital advertising, AI, streaming, and disciplined content spending. Alphabet, Meta, and Netflix all delivered significant EPS surprises, though some results included one-off items that investors should interpret with caution. Advertising remains a cyclical business, making the sector sensitive to shifts in consumer confidence, but platform models continue to generate strong cash flow. A neutral allocation is prudent—maintain exposure to high-quality compounders, but be aware that earnings strength is concentrated among a few leaders.

Figure 3: The Communications Services Sector Composite.

Energy — Modestly Underweight

Energy sector indicators look more constructive than their overall portfolio weight might imply, but the group remains highly sensitive to geopolitical shifts and commodity price swings. Bullish signals include relative strength, overbought/oversold measures, sector breadth, moving-average crossovers, rig counts, crude supply metrics, and spot price trends. In contrast, bearish readings are seen in crude price Bollinger bands, free cash flow yield momentum, rolling volatility, and U.S. dollar trends.

Macro forces are now more supportive of headline energy revenues. April’s CPI uptick was driven in part by a 17.9% year-over-year increase in energy costs and a 28.4% jump in gasoline prices. However, rising energy prices act as a drag on consumer spending and may eventually dampen demand, while also squeezing margins in sectors that rely heavily on energy.

FactSet’s data presents a mixed earnings picture for Energy. The sector posted the third-largest aggregate EPS surprise at +19.9%, led by Phillips 66, Marathon Petroleum, Occidental, Chevron, and Valero. However, Energy was the only sector to see Q1 earnings growth decline from March 31 estimates, and revenue beat rates were among the lowest. The sector trades at a modest 13.2 forward P/E and boasts one of the highest implied target-price upsides. The modest underweight here is driven by cyclicality, estimated volatility, and concerns about free cash flow momentum, rather than valuation. Moreover, a “deal” with Iran would likely remove the war premium from energy prices and negatively impact the sector’s prospects.

Figure 4: The Energy Sector Composite.

Financials — Underweight

Financials are supported by a solid earnings base, but their relative-indicator profile is weak. Key indicators are negative, including relative price trend, overbought/oversold conditions, sector volatility, maximum relative drawdown, economic surprises, the U.S. dollar, investment-grade OAS, forward earnings yield, and the yield curve. Offsetting positives include the total-return trend and growth in bank loans, while relative-strength momentum and business credit conditions hold steady.

Earnings results outshine the sector’s indicator profile. FactSet notes Financials’ earnings growth climbed to 21.8% from 14.8% since March 31, driven by strong EPS beats from JPMorgan Chase, Allstate, Citigroup, Bank of America, and Morgan Stanley. Revenue growth also rose to 10.9%, buoyed by Citigroup, Morgan Stanley, and JPMorgan Chase. With a forward P/E of 14.5—among the S&P 500’s lowest—the sector remains relatively attractively valued.

Macro sensitivity is the key challenge. While a 4.3% unemployment rate is manageable, declining labor-market participation and persistent inflation complicate Fed policy and could keep funding costs high. Watchpoints remain credit costs, deposit betas, and capital-market activity. An underweight stance is justified until the yield curve, credit spreads, and economic surprises turn more favorable.

Figure 5: The Financials Sector Composite.

Health Care — Underweight

Health Care remains a defensive sector, but it has yet to reclaim market leadership. Most indicators are negative—relative price trend, 100-day breadth, sector trend, maximum relative drawdown, medical CPI, and health-care personal expenditures—while positives include relative-strength momentum, health-care construction, and book yield. Momentum reversal measures are currently neutral.

FactSet points to strong execution at the company level within Health Care, but weak overall earnings growth. The sector achieved an 89% EPS beat rate, with major positive revenue surprises from CVS Health, Centene, UnitedHealth, Eli Lilly, Cigna, and Elevance Health. Despite these successes, Health Care was the only S&P 500 sector to record a year-over-year decline in Q1 earnings, and analysts sharply reduced Q2 EPS estimates in April and May.

The challenge for the sector is that defensive demand alone cannot offset uncertainty around policy, reimbursement, utilization, and pipeline prospects. GLP-1 and specialty pharma names remain secular winners, but managed care and some services still face margin pressures and regulatory scrutiny. FactSet reports analysts forecast the largest 12-month upside for Health Care at 18.4%, with a high Buy rating share of 64%, suggesting some pessimism may already be priced in. Maintain an underweight stance on broad exposure, but consider targeted positions in innovators and firms with clear positive earnings revisions.

Figure 6: The Health Care Sector Composite.

Industrials — Underweight

Industrials display a surprisingly weak indicator profile despite solid earnings. Most readings are bearish—relative price momentum, price trend, volatility, RSI, sales yield, oil futures, and broad commodity trends—while sector cash-flow yield, fewer new lows, the U.S. dollar, and U.S. industrial production are positive. Consumer confidence trends are neutral.

Fundamentals for Industrials look a little better. FactSet shows sector earnings growth improved to 20.9% from 3.1% since March 31, aided notably by GE Vernova’s large M&A-related EPS gain. Revenue growth climbed to 8.1%, with Caterpillar and GE Aerospace providing strong positive surprises.

Macro conditions are mixed for Industrials. April’s ISM Manufacturing index was expansionary at 52.7, and S&P Global’s manufacturing PMI rose to 54.0, signaling improved factory activity. Still, rising energy costs and softened consumer confidence could pressure transportation, machinery, and cyclical orders. The sector benefits from long-term themes like aerospace backlogs, electrification, reshoring, and infrastructure investment, but much of this is already priced into leading names. Underweighting remains prudent while momentum lags. Favor aerospace, electrical equipment, and automation over lower-margin transport and short-cycle cyclicals.

Figure 7: The Industrials Sector Composite.

Information Technology — Overweight

Technology continues to stand out as the strongest fundamental leader, with most indicators supporting an overweight stance. Relative momentum, both overbought/oversold measures, sales yield, short interest, and earnings-revision breadth all register as bullish. The sole negative is market-based inflation expectations.

Earnings results for Information Technology are exceptional. FactSet notes the sector had the highest Q1 earnings growth at 54.3%, with every industry posting increases. Semiconductors and semiconductor equipment soared 107%, led by NVIDIA and Micron; excluding those two, sector growth was still robust at 30.1%. Revenue growth also topped all sectors at 31.7%, with every industry advancing—semiconductors at 54%, and hardware/storage/peripherals at 34%.

Recent results from NVIDIA, Microsoft, Apple, Dell, Intel, Salesforce, and HP have driven upgrades to earnings and revenue estimates for the sector. The main risks are valuation and interest-rate sensitivity: the S&P 500’s forward P/E is already 21.2, and renewed inflation could keep discount rates elevated. Nonetheless, strong AI infrastructure spending, software monetization, cloud growth, and upward earnings revisions support an overweight. Prioritize companies turning AI demand into tangible revenue, margin gains, and free cash flow over those trading purely on AI hype.

Figure 8: The Information Technology Sector Composite.

Materials — Underweight

Materials show some improvement in macro-sensitive indicators, but broader trends remain weak. Key indicators are bearish for the relative price moving-average cross, price trend, momentum, deviation from trend, silver, gold, and earnings yield. Positive signals come from volatility, emerging-versus-developed equity momentum, copper momentum, natural-gas mean reversion, sales yield, and industrial production, while overbought/oversold readings are neutral.

FactSet reports Q1 earnings growth for Materials was a robust 42.5%, the third-highest among all sectors, mainly due to Metals & Mining. Excluding that industry, growth would have been 14.6%. The group also posted a healthy 3.3% aggregate revenue surprise. However, only 73% of Materials companies beat EPS estimates—one of the lowest rates in the sector—and most trend indicators remain bearish.

Macro signals are mixed. Manufacturing gauges have improved—April ISM Manufacturing came in at 52.7 and S&P Global’s PMI at 54.0, which is constructive for chemicals, metals, and packaging. However, higher energy costs could pressure margins, and China/global demand remain key drivers for commodity-linked stocks. Analysts forecast a solid 12-month upside of 17.9% and a high 64% Buy-rating share for the sector, according to FactSet. Maintain selective exposure to copper, electrification, and cost-disciplined specialty materials, but remain broadly underweight.

Figure 9: The Materials Sector Composite.

Real Estate — Neutral

Real Estate remains highly sensitive to interest rates, with some improvement in breadth but unresolved macro headwinds. Indicators are bearish for relative price trend, positive days, deviation from trend, homebuilding, and Citi economic surprise. On the positive side, 50-day breadth, unemployment data, the 30-year Treasury yield, construction-supplies industrial production, and small-business credit conditions suggest a more balanced outlook than the price trend alone implies.

Macro headwinds are evident. April new-home sales declined 6.2% to a 622,000 annualized rate, year-over-year sales dropped 11.3%, and inventory climbed to 9.4 months of supply as mortgage rates remained elevated. Persistent inflation also makes it less likely that rates will drop quickly, impacting REIT discount rates, cap rates, and financing costs.

FactSet highlights that Real Estate posted a 74% EPS beat rate—one of the sector’s lowest—and the smallest projected 12-month upside at 10.6%. Net profit margins also declined year over year, with real estate showing the largest margin deterioration of all 11 sectors. A neutral stance remains prudent: the sector could rebound if rates fall, but current fundamentals are uneven. Favor data centers, industrial/logistics, and select necessity retail, while remaining cautious on office and highly leveraged REITs.

Figure 10: The Real Estate Sector Composite.

Utilities — Modest Overweight

Utilities present a mixed technical backdrop, but enjoy positive fundamental and thematic support. Bearish indicators include relative moving-average cross, reversals, overbought/oversold measures, deviation from trend, crude oil, the earnings-yield spread versus the 10-year Treasury, and manufacturing PMI. Bullish signals come from relative momentum, 50-day breadth, capacity utilization, and dividend yield, with the copper/gold ratio holding neutral.

The earnings and revenue performance for Utilities is stronger than generally expected. FactSet reports Utilities delivered the largest aggregate revenue surprise at 7.3% and the third-highest sector revenue growth at 14.3%, with all five industries showing year-over-year gains. Independent Power & Renewable Electricity Producers led with 29% growth, trailed by Electric Utilities at 15% and Multi-Utilities at 11%.

The investment thesis for Utilities now extends beyond defensiveness or yield. It increasingly captures electricity demand growth from AI data centers, grid investment, electrification, and regulated capital spending. The primary risk remains interest rates: if inflation stays high and Treasury yields climb, dividend proxies may underperform. April’s CPI jump to 3.8% bears watching. Even so, Utilities offer earnings visibility, lower economic sensitivity, and exposure to rising power demand within a portfolio. Favor companies with supportive regulation, visible rate-based growth, and strong balance sheets.

Figure 11: The Utilities Sector Composite.

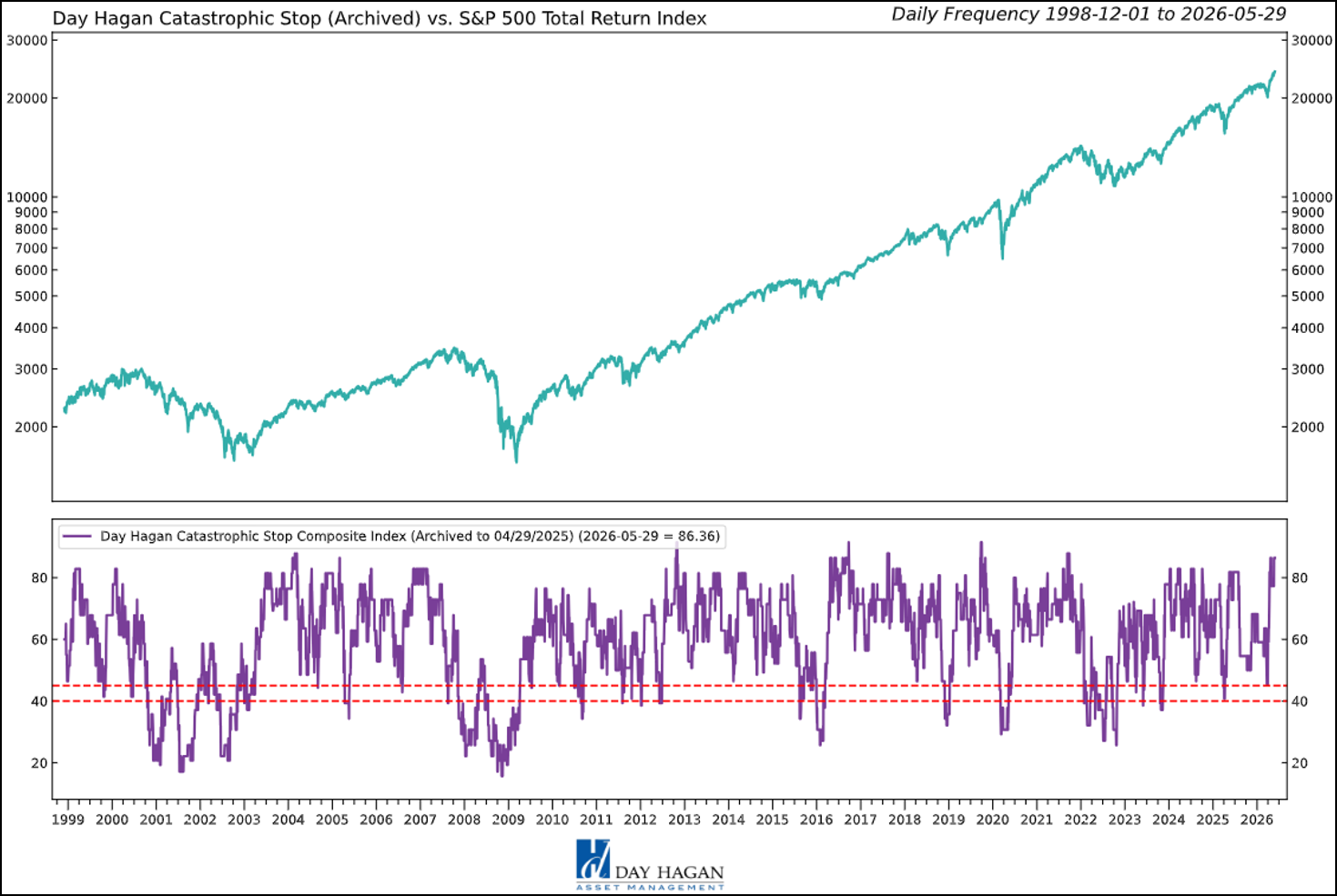

Catastrophic Stop Update

The Catastrophic Stop model combines time-tested, objective indicators designed to identify high-risk periods for the equity market. The model entered June recommending a fully invested equity allocation relative to the benchmark.

The weight of the evidence suggests that any weakness is unlikely to extend into a significant downtrend at this time. If our model triggers a sell signal (below 40% for two consecutive days), indicating more substantial problems, we will raise cash immediately.

Figure 12: The Catastrophic Stop model recommends a fully invested equity position (relative to the benchmark). Because the model uses indices to extend its history, it is considered hypothetical.

Hypothetical and historical past performance is not indicative of future results. There can be no assurance that any investment or strategy will achieve its objectives or avoid substantial losses or have comparable results. This information is provided for illustrative purposes only and is not a prediction, projection, or guarantee of future performance. Hypothetical results do not reflect actual trading, were derived using the benefit of hindsight, and may not reflect material economic and market events. Actual results vary and depend on many factors and subject to risk and uncertainties.

Our goal is to stay on the right side of the prevailing trend and introduce risk management when conditions deteriorate. Currently, the uptrend remains intact. The broader-based composite models, which call for U.S. and international economic growth, inflation trends, liquidity, and equity demand, remain constructive. The Catastrophic Stop model is positive, and we are aligned with its message. If our models shift to bearish levels, we will raise cash.

This strategy uses measures of price, valuation, economic trends, liquidity, and market sentiment to make objective, rational, and unemotional decisions about how much capital to allocate and where to invest it.

Day Hagan Asset Management

1000 S. Tamiami Trl

Sarasota, FL 34236

Toll Free: (800) 594-7930

Office Phone: (941) 330-1702

Website: https://dayhagan.com or https://dhfunds.com

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

Day HaganSmart Sector®

With Catastrophic Stop ETF

Symbol: SSUS

Disclosures

The data and analysis contained within are provided “as is” and without warranty of any kind, either express or implied. The information is based on data believed to be reliable, but it is not guaranteed. Day Hagan DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY, OR FITNESS FOR A PARTICULAR PURPOSE OR USE. All performance measures do not reflect tax consequences, execution, commissions, and other trading costs, and as such, investors should consult their tax advisors before making investment decisions, as well as realize that the past performance and results of the model are not a guarantee of future results. The Smart Sector® Strategy is not intended to be the primary basis for investment decisions, and the usage of the model does not address the suitability of any particular investment for any particular investor.

Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many difficulties, and their effectiveness has significant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the effectiveness of such devices. Day Hagan believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider differing viewpoints and use a weight-of-the-evidence approach that fits their investment needs.

Past performance does not guarantee future results. No current or prospective client should assume future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client’s portfolio. Historical performance results for investment indexes and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that a portfolio will match or outperform any particular benchmark. Comparisons to indices are inherently unreliable indicators of future performance. The strategies used to generate the performance vary from those used to generate the returns depicted in the benchmarks. Investors cannot directly invest in an index.

The information contained herein is provided for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The securities, instruments, or strategies described may not be suitable for all investors, and their value and income may fluctuate. Past performance is not indicative of future results, and there is no guarantee that any investment strategy will achieve its objectives, generate profits, or avoid losses.

This material is intended to provide general market commentary and should not be relied upon as individualized investment advice. Investors should consult with their financial professional before making any investment decisions based on this information.

Data and analysis are provided “as is” without warranty of any kind, either express or implied. Day Hagan Asset Management, its affiliates, employees, or third-party data providers shall not be liable for any loss sustained by any person relying on this information. All opinions and views expressed are subject to change without notice and may differ from those of other investment professionals within Day Hagan Asset Management or Ashton Thomas Private Wealth, LLC.

Accounts managed by Day Hagan Asset Management or its affiliates may hold positions in the securities discussed and may trade such securities without notice.

Day Hagan Asset Management is a division of and doing business as (DBA) Ashton Thomas Private Wealth, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training.

There is no guarantee that any investment strategy will achieve its objectives, generate dividends, or avoid losses.

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

Sector Definitions:

Sector Composite Models — Day Hagan Sector Composite Models use quantitative, rules-based indicators to evaluate relative sector conditions across trend, momentum, valuation, breadth, macroeconomic, and sentiment inputs. The models are designed to support disciplined sector allocation decisions. Hypothetical and historical past performance is not indicative of future results. There can be no assurance that any investment or strategy will achieve its objectives, avoid substantial losses, or have comparable results. This information is provided for illustrative purposes only and is not a prediction, projection, or guarantee of future performance. Hypothetical results do not reflect actual trading, were derived using the benefit of hindsight, and may not reflect material economic and market events. Actual results vary and depend on many factors and are subject to risks and uncertainties.

S&P 500 — A stock market index tracking 500 of the largest publicly traded U.S. companies; commonly used as a benchmark for the overall U.S. equity market.

Dow Jones Industrial Average (DJIA) — A price-weighted stock index of 30 large U.S. companies, often used as a headline measure of the stock market.

Nasdaq Composite — A stock market index that includes thousands of stocks listed on the Nasdaq exchange, with heavy exposure to technology companies.

PMI (Purchasing Managers’ Index) — A survey-based economic indicator that measures business activity; readings above 50 generally indicate expansion, while readings below 50 indicate contraction.

ISM (Institute for Supply Management) Index — A widely followed U.S. manufacturing activity index based on purchasing manager surveys; used to gauge economic momentum.

CPI (Consumer Price Index) — A measure of inflation that tracks changes in the prices consumers pay for goods and services.

Medical CPI — A CPI subcategory that measures inflation specifically in medical care goods and services.

Federal Reserve (the Fed) — The central bank of the United States, responsible for setting monetary policy and influencing interest rates and financial conditions.

Benchmark weighting — The percentage weight a sector or asset has in a benchmark index, used as a reference point for portfolio positioning.

Overweight — A portfolio position above the benchmark weighting, reflecting a more favorable view of that sector or asset.

Underweight — A portfolio position below the benchmark weighting, reflecting a less favorable view of that sector or asset.

Neutral — A portfolio position roughly in line with the benchmark weighting, indicating no strong directional preference.

Sector rotation — A market dynamic in which investors shift money between sectors based on changing economic, interest-rate, or earnings expectations.

Relative strength — A measure of how a stock, sector, or asset performs compared with a benchmark or another asset.

Breadth — A technical measure showing how broadly market participation is spread, such as how many stocks in a sector are advancing or hitting new highs/lows.

RSI (Relative Strength Index) — A technical momentum indicator used to assess whether an asset may be overbought or oversold.

Yield curve — The relationship between yields on short- and long-term Treasury securities; changes in its shape can signal shifts in economic expectations.

10Y-2Y spread — The difference between the 10-year and 2-year U.S. Treasury yields, often used as a quick measure of the yield curve’s steepness.

WTI crude — West Texas Intermediate crude oil, a key U.S. benchmark price for oil.

REITs (Real Estate Investment Trusts) — Companies that own, operate, or finance income-producing real estate and typically trade like stocks.

Communication Services sector: The Communication Services Sector includes telecom and media & entertainment companies including producers of interactive gaming products and companies engaged in content and information creation or distribution through proprietary platforms.

Consumer Discretionary sector: The Consumer Discretionary sector's manufacturing segment includes automobiles & components, household durable goods, leisure products and textiles & apparel. The services segment includes hotels, restaurants, and other leisure facilities. It also includes distributors and retailers of consumer discretionary products.

Consumer Staples sector: The Consumer Staples sector includes manufacturers and distributors of food, beverages and tobacco and producers of non-durable household goods and personal products. It also includes distributors and retailers of consumer staples products including food & drug retailing companies.

Energy sector: The Energy sector includes companies that operate in the areas of exploration & production, refining & marketing, and storage & transportation of oil & gas and coal & consumable fuels. It also includes companies that offer oil & gas equipment and services.

Financials sector: The Financials sector includes banking, financial services, consumer finance, capital markets and insurance activities. It also includes Financial Exchanges & Data and Mortgage REITs.

Fixed Income sector: The Fixed Income sector includes investment securities that pay investors fixed interest payments until the maturity date. Designed for income generation and capital preservation, this sector includes government bonds, corporate bonds, municipal bonds and certificates of deposit (CDs).

Health Care sector: The Health Care sector includes health care providers & services, health care equipment & supplies, and health care technology companies. It also includes companies involved in the research, development, production and marketing of pharmaceuticals and biotechnology products.

Industrials sector: The Industrials sector includes aerospace & defense, building products, electrical equipment and machinery and companies that offer construction & engineering services. It also includes providers of commercial & professional services including printing, environmental and facilities services, office services & supplies, security & alarm services, human resource & employment services, research & consulting services. It also includes companies that provide transportation services.

Information Technology sector: The Information Technology sector includes software and information technology services, manufacturers and distributors of technology hardware & equipment such as communications equipment, cellular phones, computers & peripherals, electronic equipment and related instruments, and semiconductors and related equipment & materials.

Materials sector: The Materials sector includes chemicals, construction materials, forest products, glass, paper and related packaging products, and metals, minerals and mining companies, including producers of steel.

Real Estate sector: The Real Estate sector includes companies engaged in real estate development and operation. It also includes companies offering real estate related services and Equity Real Estate Investment Trusts (REITs).

© 2026 Day Hagan Asset Management