Day Hagan Smart Sector® with Catastrophic Stop Strategy Update May 2026

A downloadable PDF copy of the Article:

Day Hagan Smart Sector® with Catastrophic Stop Strategy Update May 2026 (pdf)

Executive Summary

In April, the U.S. stock market was supported by robust corporate earnings, renewed interest in artificial intelligence, and economic data that signaled ongoing growth. The Nasdaq, S&P 500, and Dow all posted strong gains for the month, led primarily by large-cap technology, software, semiconductor, and AI-related companies. While gains were concentrated among leading sectors, this leadership helped lift the broader market. However, the market environment also reflected the Federal Reserve's ongoing caution amid persistent inflationary pressures.

Strong first-quarter earnings were a key driver. According to FactSet, as of May 1, S&P 500 companies reported blended earnings growth of 27.1% and revenue growth of 11.1%. Leading sectors included Communication Services, Information Technology, and Consumer Discretionary. Additionally, seven sectors saw double-digit earnings increases, helping to offset concerns about rising input costs and geopolitical uncertainty.

The broader economic environment was mixed. March Consumer Price Index (CPI) data showed inflation rising 3.3% year over year and 0.9% from the previous month. Energy prices increased 10.9%, driven by a notable 21.2% rise in gasoline prices, highlighting oil price shocks as a risk to corporate margins, consumers, and interest rates. The Federal Reserve maintained its benchmark rate at 3.50%–3.75% on April 29, emphasizing its data-dependent approach in future policy decisions.

Economic growth data continued to support equities. First-quarter GDP grew at a 2.0% annualized rate, with March personal spending up 0.9% and PCE inflation at 3.5% year over year. Manufacturing activity in April remained in expansion territory, as indicated by an ISM reading of 52.7, though input cost pressures were evident, with the prices-paid index reaching its highest level since April 2022.

In summary, companies demonstrating strong earnings, exposure to artificial intelligence trends, and the ability to adjust prices benefited most in April. However, inflation, energy costs, and central bank policy remain important factors for investors to monitor.

Sector

Consumer Discretionary

Consumer Staples

Communication Services

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Real Estate

Utilities

Outlook (relative to benchmark weighting)

Modest Overweight

Underweight

Overweight

Modestly Underweight

Underweight

Underweight

Underweight

Overweight

Neutral

Overweight

Overweight

Sector Review

The current portfolio takes a balanced approach, favoring both growth and defensive areas while reducing exposure to traditional cyclical sectors. Overweights in Information Technology and Communication Services reflect a tilt toward long-term growth themes such as artificial intelligence, software, and digital platforms, as well as companies with strong earnings momentum. This positioning may benefit the portfolio if investor risk appetite is steady and earnings trends remain positive.

Simultaneously, higher allocations to Utilities and Real Estate indicate a preference for income and stability, which may provide support if bond yields fall or if the market shifts toward more defensive, dividend-focused sectors. Underweights in Financials, Industrials, Energy, Health Care, and Consumer Staples show less conviction in economic cyclicals, commodity-driven earnings, banks, and traditional defensive stocks. The reduced exposure to Energy is particularly notable should inflation or oil prices rise, while the Financials underweight may reflect concerns about credit conditions or slower lending growth.

Overall, this portfolio is designed for an environment where growth leadership continues but also provides a measure of protection through defensive, income-oriented sectors. While it may underperform if value stocks, banks, energy, or industrials take the lead, it stands to do well if themes such as AI-driven growth, lower yields, and quality balance sheets remain prominent.

Consumer Discretionary: Consumer Discretionary has a positive technical setup, led by bullish relative strength across short- and intermediate-term moving averages, trend deviation, price momentum, and overbought/oversold measures. That supports an overweight view, but the signal set is not unanimous. Weak relative 120-day net new highs show narrow participation, and relative forward P/E remains a headwind.

The fundamental picture is also mixed but improving. Q1 2026 earnings were strong, with a median reported growth of 45.9% and a 33.6% median surprise (to date). Expectations slow from there, with Q2 growth of 7.7%, fiscal 2026 growth of 15.3%, and fiscal 2027 growth of 17.0%. Revisions are positive for Q2 but slightly negative for 2026 and 2027, so the estimate momentum is not yet broad-based. Valuation is the main constraint: the sector trades at 25.1x forward earnings, well above the S&P 500’s 19.9x.

Macro inputs are also not one-sided. Consumer credit trends remain supportive for spending, but housing is only neutral. March housing starts rose sharply, while permits fell, pointing to uneven housing-linked demand. The 30-year Treasury yield finished April at 4.98%, a level that remains a risk to big-ticket spending. Overall, Consumer Discretionary merits a modest overweight, with position size reflecting high valuation and uneven breadth

Figure 1: The Consumer Discretionary sector is in minor oversold territory. A reversal back above the lower SD bracket would generate a buy signal, potentially indicating renewed investor demand. (Note: All charts are proprietary from Day Hagan Asset Management.)

Consumer Staples: Consumer Staples has a weak relative setup. Price momentum is the only clear technical positive, while other moving-average trends, deviation from trend, overbought/oversold measures, relative net new highs, and 45-day relative breadth are all negative. That points to poor participation and limited sponsorship, even though the sector can still benefit when financial conditions are loose or economic surprises weaken.

The earnings picture is stable but not compelling. Q1 2026 median reported growth was 3.6% (to date), with a 3.3% median surprise. Q2 expected growth improves to 7.3%, while fiscal 2026 and fiscal 2027 expected growth are 8.0% and 8.8%, respectively. Revisions are not strong enough to offset weak price action: Q2 revisions are positive, but 2026 and 2027 revision ratios are only slightly positive to negative. Valuation is also not cheap, with the sector at 22.5x forward earnings, above the S&P 500’s 19.9x.

Macro data are mixed. Financial conditions remain supportive, with the Chicago Fed NFCI at -0.52 in the week ended April 24, indicating looser-than-average conditions. But food inflation is no longer a major tailwind: March food CPI was up 2.7% year over year, with food at home up 1.9% and food away from home up 3.8%. That reduces pricing power versus prior years. Overall, Staples are underweight: defensive characteristics help in risk-off periods, but weak breadth, poor relative strength, and full valuation limit upside.

Figure 2: Relative breadth has not yet turned positive for the Consumer Staples sector.

Communication Services: Communication Services has a constructive setup, but the signal is not one-sided. Relative strength is above key moving-average measures, and both overbought/oversold indicators are bullish. Relative earnings yield is also supportive, suggesting the sector is not expensive relative to its earnings base. The main technical concern is a relative price deviation from trend, which has turned bearish and suggests some risk that the recent move may be extended. The yield-curve indicator is also bearish; the 10-year minus 2-year Treasury spread averaged 0.52% in April, down slightly from 0.54% in March, so the curve remains positive but flatter.

The earnings backdrop is strong. Q1 2026 median reported growth (to date) was 64.6%, with a 70.9% median surprise, the strongest profile among the major sectors in the uploaded data. Q2 growth is expected to be lower but still solid at 16.9%. Full-year expectations are 25.8% growth for 2026 and 8.3% for 2027. Revisions are favorable for Q2, with a revisions ratio of 0.83, but momentum slows for the out years, with a 0.21 ratio for 2026 and -0.03 for 2027.

Valuation is reasonable versus growth. The sector trades at 19.6x forward earnings, roughly in line with the S&P 500’s 19.9x, while offering better near-term earnings growth. Overall, Communication Services merits an overweight rating, but the case depends on continued earnings delivery and broader participation following a strong run

Figure 3: Intermediate-term trend indicators showing signs of stress. We’re monitoring closely for signs that a downgrade is warranted.

Energy: Energy has a constructive but volatile profile. Relative strength, sector breadth, moving-average crossovers, world rig count, crude spot price, and the weaker-dollar backdrop are supportive. That is a different setup from more rate- or consumer-sensitive sectors: the case is tied more directly to commodity pricing, supply discipline, and cash-flow durability. The main offsets are overbought/oversold conditions, high rolling volatility, negative free cash flow yield momentum, and still-elevated crude days of supply (in the U.S.).

The earnings data are strong. Q1 2026 median reported growth was 14.6%, with a 9.4% median surprise and 90.0% of companies reporting positive surprises. The forward numbers are much stronger near term: Q2 expected growth is 94.7%, fiscal 2026 expected growth is 50.3%, and fiscal 2027 expected growth slows to 0.8%. Revisions are supportive, with positive revision ratios in Q2 2026 and 2027. Valuation is not the bargain it often is for Energy: the sector trades at 21.1x forward earnings, above the S&P 500’s 19.9x.

Macro and commodity inputs are mixed. WTI was near $99.89 on April 27, while U.S. crude days of supply were 28.6 for the week ended April 24. Worldwide rigs fell to 1,715 in April from 1,791 in March, suggesting some continued supply restraint. The trade-weighted dollar also weakened through April, a trend that usually helps commodities. Overall, Energy merits a neutral-to-modestly-underweight allocation given the run-up and overbought conditions, but it should be sized for volatility and monitored closely if crude rolls over.

Figure 4: Last month, we wrote that the energy sector is benefiting from geopolitical upheavals, even as supply remained above normal. The latest update shows inventories being drawn down.

Financials: Financials have a weaker setup. The main positive is relative momentum, with lower sector volatility and bank loan growth also supportive. Most other inputs are negative, including relative price trend, total return trend, overbought/oversold conditions, maximum relative drawdown, business credit conditions, financial-institution credit spreads, forward earnings yield, the dollar, economic surprises, and the yield curve. That combination argues against a broad overweight, even though parts of the sector may still benefit from loan growth and a still-positive curve.

Earnings are improving, but not enough to offset the weaker indicator profile. Q1 2026 median reported growth was 23.2%, with a 5.2% median surprise. Q2 expected growth is 9.8%, while fiscal 2026 and 2027 expected growth are 11.9% and 11.3%. Revisions are soft: the Q2 revisions ratio is only 0.17, and 2026 is slightly negative at -0.01. Valuation is relatively positive at 12.9x forward earnings, well below the S&P 500’s 19.9x, but the lower multiple looks partly justified by weaker breadth and credit sensitivity.

Macro inputs are not favorable. The 10-year minus 2-year Treasury spread averaged 0.52% in April, positive but flatter than in March, which limits the net interest margin tailwind. Bank loans and leases were still growing through mid-April, but credit conditions and financial-sector spreads remain watch points. Overall, Financials should remain underweighted.

Figure 5: Business credit conditions showing signs of stress.

Healthcare: Health Care remains underweight. The sector has poor relative price trends, weak relative momentum, negative 100-day relative breadth, and a bearish sector trend. Maximum relative drawdown is also negative, which means the sector is not just lagging but doing so with poor downside participation. The only clear valuation-related support is book yield. Health care construction is neutral, but the macro indicators tied to medical CPI and health care personal expenditures are not helping relative performance.

The earnings profile is steady, but not strong enough to offset weak price action. Q1 2026 median reported growth was 24.3%, with a 7.7% median surprise and 90.9% positive surprises. Q2 expected growth is 10.9%, while fiscal 2026 and fiscal 2027 expected growth are 12.7% and 16.5%. Revisions are positive for Q2, 2026, and 2027, which is a relative bright spot. Valuation is reasonable at 18.1x forward earnings, below the S&P 500’s 19.9x, but the discount is not enough to overcome weak relative trends.

Macro data are mixed. Medical care CPI fell 0.2% in March, after rising 0.5% in February, with prescription drugs down 1.5%. Health care services spending remained large and growing, reaching $3.72 trillion annualized in Q1 2026, up from $3.65 trillion in Q4 2025. Overall, Health Care has improving earnings support, but weak technicals and poor relative sponsorship argue for staying underweight.

Figure 6: Health Care’s relative momentum has continued to deteriorate from last month’s update. However, it is now in oversold territory, and a reversal would be constructive.

Industrials: Industrials have a weaker relative setup despite some macro support. Relative price momentum, relative price trend, sector volatility, RSI, and sales yield are all negative. Oil exposure is also a headwind, which matters for transportation and other fuel-sensitive industries. The positives are more cyclical: fewer 210-day new lows, supportive cash-flow yield, a weaker dollar, firm commodity trends outside oil, and a positive signal from U.S. industrial production. Consumer confidence is neutral, which keeps the demand backdrop from becoming clearly bullish.

Earnings are solid but not accelerating enough to overcome the weak technical picture. Q1 2026 median reported growth was 23.3%, with a 10.6% median surprise and 86.2% positive surprises. Q2 expected growth is 18.4%, while fiscal 2026 and fiscal 2027 expected growth are 14.1% and 24.1%. Revisions are favorable, with positive ratios for Q2, 2026, and 2027, so analysts are still raising estimates. Valuation is a constraint: the sector trades at 24.0x forward earnings, well above the S&P 500’s 19.9x.

The macro data are mixed. Industrial production fell 0.5% in March but still rose at a 2.4% annualized rate in Q1; manufacturing output slipped 0.1% in March but rose at a 3.0% annualized rate in Q1. Consumer confidence improved slightly to 92.8 in April but remained low. Overall, Industrials should be modestly underweight: earnings and revisions are good, but relative trends are weak, and upside is potentially limited by extended multiples.

Figure 7: Relative price momentum is negative.

Information Technology: Information Technology has one of the cleaner sector setups. Relative price momentum is bullish; both overbought/oversold measures are positive; sales yield is supportive; short interest is favorable; and earnings revision breadth is bullish. The main negative is market-based inflation expectations. That matters because Technology is a long-duration sector; when inflation expectations rise, valuation sensitivity usually increases.

The earnings backdrop is the main reason to stay constructive. Q1 2026 median reported growth was 15.2%, with a 4.4% median surprise. The quality of results was strong: 96.4% of reporting companies posted positive surprises, with no negative surprises in the data. Forward growth is much stronger than the trailing quarter. Q2 expected growth is 59.6%, fiscal 2026 expected growth is 47.6%, and fiscal 2027 expected growth is 29.1%. Revisions are also supportive, with positive revision ratios for Q2, 2026, and 2027, confirming that estimates are still moving higher.

Valuation is not cheap, but it is easier to justify here than in sectors with weaker growth. Technology trades at 20.4x forward earnings, only modestly above the S&P 500’s 19.9x, despite much faster expected earnings growth. The risk is inflation. The 10-year breakeven inflation rate averaged 2.38% in April, up from 2.34% in March, supporting the bearish inflation expectations signal. Overall, Technology remains an overweight, supported by earnings revisions, strong growth, and broad technical confirmation.

Figure 8: Short interest has moved lower as shorts covered into last month’s rally.

Materials: The Materials composite is mixed and leans neutral. The sector has support from the relative moving-average cross, overbought/oversold work, deviation from trend, lower sector volatility, copper momentum, natural gas mean reversion, and sales yield. That is a more commodity-sensitive and cyclical profile than Consumer Staples or Health Care, but the positives are offset by bearish relative price trend and momentum, weaker emerging-market versus developed-market equity momentum, poor silver and gold momentum, weak earnings yield, and a negative signal from industrial production for materials.

The earnings picture is better than the relative price trend suggests. Q1 2026 median reported growth was 32.8%, with a 7.4% median surprise and 80.0% positive surprises. Q2 expected growth is 25.7%, fiscal 2026 expected growth is 35.3%, and fiscal 2027 expected growth is 11.1%. Revisions are mixed: Q2 is positive, but 2026 and 2027 revisions are slightly negative. Valuation is reasonable but not deeply discounted, with the sector at 18.7x forward earnings, below the S&P 500’s 19.9x.

Macro support is uneven. Copper has been the main positive commodity, while the momentum of precious metals has weakened. Industrial production was also a headwind: total output fell 0.5% in March, and materials output fell 0.6%, led by consumer parts and energy materials. Overall, Materials has improving earnings and fair valuation, but weak relative momentum and soft production data argue for a neutral stance.

Figure 9: The Materials sector reversed from a significant overbought condition, reached oversold levels, and is now back to neutral.

Real Estate: Real Estate remains modestly underweight. The sector’s relative price trend and percentage of positive days are bearish, and the homebuilding signal is negative, which is important because housing-related sentiment often drives investor interest in the group. Credit conditions are also a headwind, and the economic-surprise signal is bearish. The positives are more macro-sensitive: 50-day relative breadth has improved, unemployment data remain supportive, and industrial production of construction supplies has improved.

The earnings profile is better than the price action. Q1 2026 median reported growth was 53.3%, with a 23.9% median surprise and 80.8% positive surprises. Q2 expected growth is 15.6%, with fiscal 2026 and 2027 expected growth of 20.9% and 13.7%. Revisions are mixed: Q2 is positive, 2026 is slightly negative, and 2027 is mildly positive. Valuation is the main issue. Real Estate trades at 33.1x forward earnings, the highest multiple among the major sectors in the uploaded data and well above the S&P 500’s 19.9x.

Macro data are mixed. The unemployment rate was 4.3% in March, and construction added 26,000 jobs, supporting the labor signal. Construction supplies output rose to 100.08 in March from 99.66 in February. But the 30-year Treasury yield ended in April at 4.98%, still high in absolute terms, and small-business optimism fell to 95.8, with capital outlay plans at their lowest level since 2009. Overall, Real Estate has improving earnings but weak relative trends and expensive valuation.

Figure 10: Relative breadth is still weak.

Utilities: Utilities remain underweight despite a few defensive supports. Relative price moving-average trends, reversals, momentum, overbought/oversold measures, and deviation from trend are all negative, indicating weak sponsorship. The sector does have improving 50-day relative breadth, a supportive dividend yield signal, and a bullish input from crude oil futures, which helps when energy costs are less of a pressure point. But the earnings-yield spread relative to the 10-year Treasury is bearish, so the sector’s income appeal remains constrained by competing bond yields.

The earnings profile is better than the price action, but not strong enough to change the call. Q1 2026 median reported growth was 3.9%, with a 2.6% median surprise. Q2 expected growth improves to 17.8%, while fiscal 2026 and fiscal 2027 expected growth are 15.8% and 9.5%. Revisions are mixed: Q2 revisions are negative, 2026 is only slightly positive, and 2027 is modestly positive. Valuation is not compelling for a defensive sector. Utilities trade at 19.1x forward earnings, only slightly below the S&P 500’s 19.9x, while offering lower long-term growth.

Macro inputs are also a headwind. The ISM Manufacturing PMI held at 52.7 in April, indicating expansion, but employment contracted and input costs rose sharply. Capacity utilization fell to 75.7% in March, with utilities utilization at 70.3%, well below its long-run average. Overall, Utilities look defensive but not attractive enough for an overweight; weak relative trends and rate sensitivity argue for underweight.

Figure 11: Relative price momentum showing signs of nearing resistance.

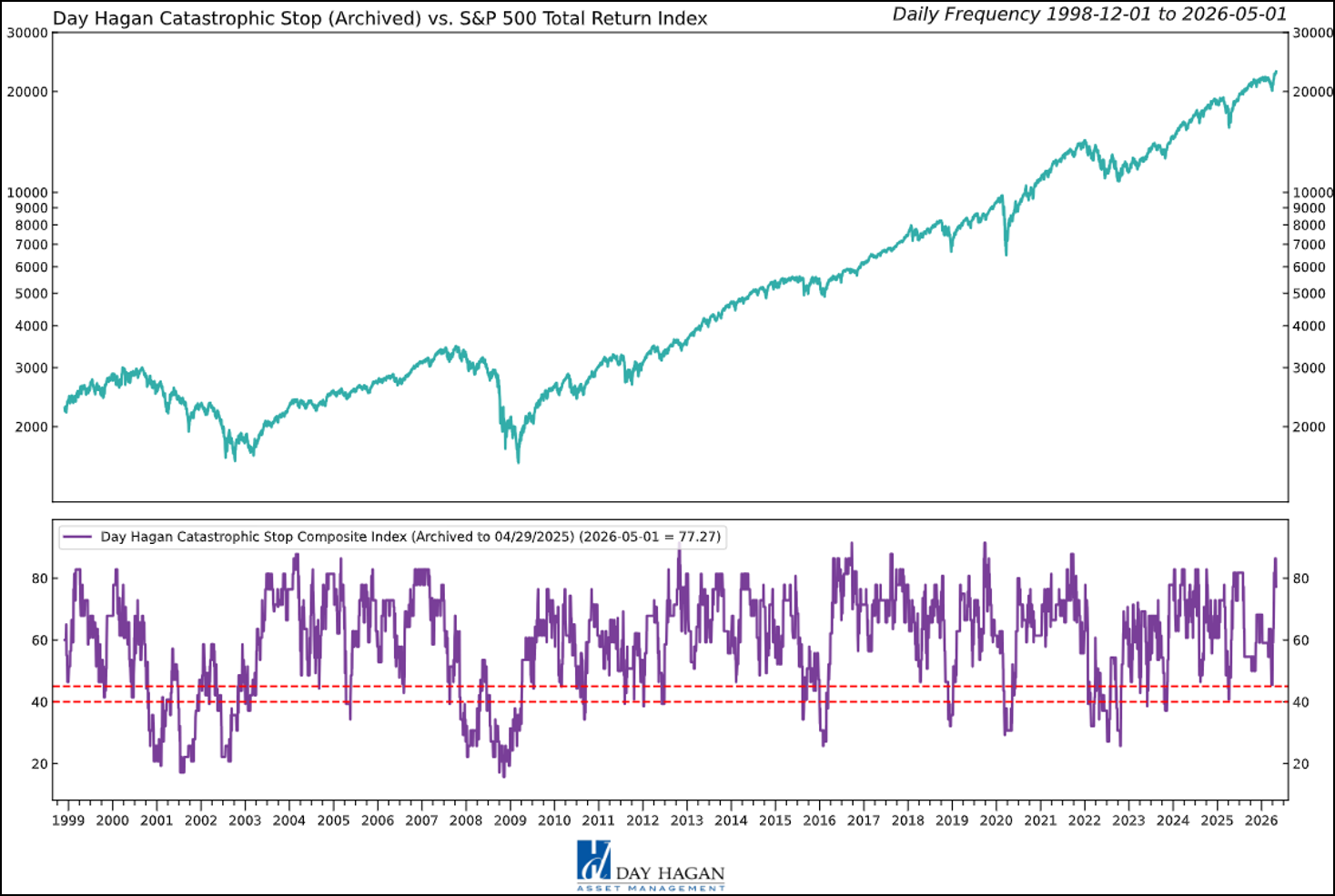

Catastrophic Stop Update

The Catastrophic Stop model combines time-tested, objective indicators designed to identify high-risk periods for the equity market. The model entered May recommending a fully invested equity allocation relative to the benchmark.

The weight of the evidence suggests that any weakness is unlikely to extend into a significant downtrend at this time. Of course, if our model triggers a sell signal (below 40% for two consecutive days), indicating more substantial problems, we will raise cash immediately.

Figure 12: The Catastrophic Stop model recommends a fully invested equity position (relative to the benchmark). Because the model uses indices to extend its history, it is considered hypothetical.

Hypothetical and historical past performance is not indicative of future results. There can be no assurance that any investment or strategy will achieve its objectives or avoid substantial losses or have comparable results. This information is provided for illustrative purposes only and is not a prediction, projection, or guarantee of future performance. Hypothetical results do not reflect actual trading, were derived using the benefit of hindsight, and may not reflect material economic and market events. Actual results vary and depend on many factors and subject to risk and uncertainties.

This chart compares the S&P 500 with the Day Hagan Daily Market Sentiment Composite. The current composite reading is 89.43, well above the +70 upper bracket, indicating elevated or optimistic sentiment. Historically, readings above this level often suggest a strong risk appetite and a positive market tone, but they can also indicate the market is becoming stretched in the short term. This is not necessarily bearish by itself; rather, it suggests investors are already leaning bullish, so near-term upside may be more vulnerable to consolidation, volatility, or disappointment. The way we incorporate these types of models into our outlook is to "Go with the flow until it reaches an extreme and reverses." We're still going with the flow, but headwinds are building.

Figure 13: A sell signal would occur if the Composite falls back below 70, suggesting investors may be shifting toward a more pessimistic view of the market.

Our goal is to stay on the right side of the prevailing trend and introduce risk management when conditions deteriorate. Currently, the uptrend remains intact. The broader-based composite models, which call for U.S. and international economic growth, inflation trends, liquidity, and equity demand, remain constructive. The Catastrophic Stop model is positive, and we are aligned with its message. If our models shift to bearish levels, we will raise cash.

This strategy uses measures of price, valuation, economic trends, liquidity, and market sentiment to make objective, rational, and unemotional decisions about how much capital to allocate and where to invest it.

Day Hagan Asset Management

1000 S. Tamiami Trl

Sarasota, FL 34236

Toll Free: (800) 594-7930

Office Phone: (941) 330-1702

Website: https://dayhagan.com or https://dhfunds.com

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

Day HaganSmart Sector®

With Catastrophic Stop ETF

Symbol: SSUS

Disclosures

The data and analysis contained within are provided “as is” and without warranty of any kind, either express or implied. The information is based on data believed to be reliable, but it is not guaranteed. Day Hagan DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY, OR FITNESS FOR A PARTICULAR PURPOSE OR USE. All performance measures do not reflect tax consequences, execution, commissions, and other trading costs, and as such, investors should consult their tax advisors before making investment decisions, as well as realize that the past performance and results of the model are not a guarantee of future results. The Smart Sector® Strategy is not intended to be the primary basis for investment decisions, and the usage of the model does not address the suitability of any particular investment for any particular investor.

Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many difficulties, and their effectiveness has significant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the effectiveness of such devices. Day Hagan believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider differing viewpoints and use a weight-of-the-evidence approach that fits their investment needs.

Past performance does not guarantee future results. No current or prospective client should assume future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client’s portfolio. Historical performance results for investment indexes and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that a portfolio will match or outperform any particular benchmark. Comparisons to indices are inherently unreliable indicators of future performance. The strategies used to generate the performance vary from those used to generate the returns depicted in the benchmarks. Investors cannot directly invest in an index.

The information contained herein is provided for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The securities, instruments, or strategies described may not be suitable for all investors, and their value and income may fluctuate. Past performance is not indicative of future results, and there is no guarantee that any investment strategy will achieve its objectives, generate profits, or avoid losses.

This material is intended to provide general market commentary and should not be relied upon as individualized investment advice. Investors should consult with their financial professional before making any investment decisions based on this information.

Data and analysis are provided “as is” without warranty of any kind, either express or implied. Day Hagan Asset Management, its affiliates, employees, or third-party data providers shall not be liable for any loss sustained by any person relying on this information. All opinions and views expressed are subject to change without notice and may differ from those of other investment professionals within Day Hagan Asset Management or Ashton Thomas Private Wealth, LLC.

Accounts managed by Day Hagan Asset Management or its affiliates may hold positions in the securities discussed and may trade such securities without notice.

Day Hagan Asset Management is a division of and doing business as (DBA) Ashton Thomas Private Wealth, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training.

There is no guarantee that any investment strategy will achieve its objectives, generate dividends, or avoid losses.

This material is for educational purposes only. Further distribution is prohibited without prior permission. Please see the information on Disclosures and Fact Sheets here: https://dhfunds.com/literature. Charts with models and return information use indices for performance testing to extend the model histories, and they should be considered hypothetical. All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

Sector Definitions:

S&P 500 — A stock market index tracking 500 of the largest publicly traded U.S. companies; commonly used as a benchmark for the overall U.S. equity market.

Dow Jones Industrial Average (DJIA) — A price-weighted stock index of 30 large U.S. companies, often used as a headline measure of the stock market.

Nasdaq Composite — A stock market index that includes thousands of stocks listed on the Nasdaq exchange, with heavy exposure to technology companies.

PMI (Purchasing Managers’ Index) — A survey-based economic indicator that measures business activity; readings above 50 generally indicate expansion, while readings below 50 indicate contraction.

ISM (Institute for Supply Management) Index — A widely followed U.S. manufacturing activity index based on purchasing manager surveys; used to gauge economic momentum.

CPI (Consumer Price Index) — A measure of inflation that tracks changes in the prices consumers pay for goods and services.

Medical CPI — A CPI subcategory that measures inflation specifically in medical care goods and services.

Federal Reserve (the Fed) — The central bank of the United States, responsible for setting monetary policy and influencing interest rates and financial conditions.

Benchmark weighting — The percentage weight a sector or asset has in a benchmark index, used as a reference point for portfolio positioning.

Overweight — A portfolio position above the benchmark weighting, reflecting a more favorable view of that sector or asset.

Underweight — A portfolio position below the benchmark weighting, reflecting a less favorable view of that sector or asset.

Neutral — A portfolio position roughly in line with the benchmark weighting, indicating no strong directional preference.

Sector rotation — A market dynamic in which investors shift money between sectors based on changing economic, interest-rate, or earnings expectations.

Relative strength — A measure of how a stock, sector, or asset performs compared with a benchmark or another asset.

Breadth — A technical measure showing how broadly market participation is spread, such as how many stocks in a sector are advancing or hitting new highs/lows.

RSI (Relative Strength Index) — A technical momentum indicator used to assess whether an asset may be overbought or oversold.

Yield curve — The relationship between yields on short- and long-term Treasury securities; changes in its shape can signal shifts in economic expectations.

10Y-2Y spread — The difference between the 10-year and 2-year U.S. Treasury yields, often used as a quick measure of the yield curve’s steepness.

WTI crude — West Texas Intermediate crude oil, a key U.S. benchmark price for oil.

REITs (Real Estate Investment Trusts) — Companies that own, operate, or finance income-producing real estate and typically trade like stocks.

All Rights Reserved. (© Copyright 2026 Day Hagan Asset Management.)

© 2026 Day Hagan Asset Management